Forecasting Energy Markets

Introduction

Over the past several years, global events have rocked the energy markets: the Covid-19 pandemic caused the price of oil to crash, while a combination of inflation and the sanctions placed on Russia due to its invasion of Ukraine have caused the price of oil and natural gas to skyrocket. As a result, it is important to be able to forecast energy markets accurately despite global uncertainty on a day-to-day basis.

With this in mind, my project aims at developing a tool that can forecast energy markets one period into the future consistently and accurately and in a time-effective manner. This tool can help local governments allocate resources in times of volatility and help investors and high-frequency traders optimize trading futures. Specifically, by pulling publicly available data, I will train different univariate models on past values to forecast next day values.

Tools

I will be creating these models using Python. In particular, I will be using the pandas and numpy libraries to clean the data, the requests and json libraries to pull and parse the data, and the sklearn library to prepare the data. I will be using a XGBoost regressor, a Support Vector regressor, and a Random Forest regressor to forecast the data.

import requests

import pandas as pd

import numpy as np

import json

import matplotlib.pyplot as plt

import itertools

import math

import datetime

import xgboost as xgb

from xgboost import XGBRegressor

from sklearn.ensemble import RandomForestRegressor

from sklearn.svm import SVR

import sklearn

from sklearn.metrics import mean_squared_error

from sklearn.model_selection import GridSearchCV

from sklearn.model_selection import cross_val_score

from sklearn.model_selection import train_test_split

from sklearn.metrics import mean_absolute_error

from pylab import rcParams

rcParams['figure.facecolor'] = 'white'

rcParams['axes.facecolor'] = 'white'

rcParams['figure.figsize'] = 12,6

Pulling Data from the U.S. Energy Information Administration

The U.S. Energy Information Administration (EIA) collects and disseminates energy data to the public to promote efficient markets, sound policy making, and public education. The EIA makes its data available through dashboards available here: https://www.eia.gov/tools/. For people who want to pull data locally, the EIA provides documentation for their API here: https://www.eia.gov/opendata/documentation.php. To pull the data, one needs to register an API key. I blurred mine out, but one can easily be obtained from their website. However, their API has several problems. The first is that when trying to determine which data to pull, the options are often hidden, making querying data tedious. Additionally, the maximum number of points that can be pulled per request is 5000 datapoints. If one wants to pull more data, they would either have to paginate or or filter their data in the API call, as opposed to in a dataframe tool, like Pandas, which would be typically more well known by the user. My first class, LoadQuery, addresses these issues.

The class LoadQuery begins by looping through the different pages available, from which the user can select which data they want while having all options available, and then choose which dataset they want to pull. Next, the user will choose the periodicity of the data, if it comes in multiple formats, as well as the type of data that they want to pull, again, if the data comes in mulitple formats. Once chosen, the program will then paginate through the queries until all data is pulled. The data is then turned into a Pandas dataframe format, which can be accessed through the .df attribute of the LoadQuery object. The dataframe will be indexed by date.

date_switch = {'annual':'%Y',

'monthly':'%Y-%m',

'daily':'%Y-%m-%d'}

class LoadQuery:

def __init__(self, header = "",page = "", key = "",data = None, frequency = None,response = None, df = None, format = None):

self.header = 'https://api.eia.gov/v2'

self.page = page ##Which page you want to access. Created by running load_page

self.key= #XXXXXXXXX

self.data = data ##The data you want to access with the query. Created by running choose_query

self.frequency = frequency

self.response = response

self.df = df

self.format = format

def load_page(self):

##When running load_page, this creates

api_url = self.header+self.page+self.key

response = requests.get(api_url)#, verify = False)

response = response.json()

if 'frequency' not in response['response'].keys():

print('Choose your id')

check = []

for i in response['response']['routes']:

print("id: ", i['id'], " Name: ", i['name'],'\r')

check.append(i['id'])

next_page = input()

if next_page not in check:

print('What you typed was not an option')

self.load_page()

else:

self.page+='/'+next_page

self.load_page()

api_url = self.header+self.page+self.key

response = requests.get(api_url)

self.response = response.json()

def choose_frequency(self):

if len(self.response['response']['frequency']) == 1:

self.frequency = self.response['response']['frequency'][0]['id']

else:

print('Choose the frequency')

check = []

for i in self.response['response']['frequency']:

check.append(i['id'])

print(i['id'])

frequency = input()

if frequency in check:

self.frequency = frequency

else:

print('What you typed was not an option')

self.choose_frequency()

def choose_data(self):

if len(self.response['response']['data'].keys()) == 1:

self.data = list(self.response['response']['data'].keys())[0]

else:

print('Choose the data type')

check = []

for i in self.response['response']['data'].keys():

check.append(i)

print(i)

data = input()

if data in check:

self.data = data

else:

print('What you typed was not an option')

self.choose_data()

def create_info(self):

api_url = self.header+self.page+self.key+'&data[]='+self.data+'&frequency='+self.frequency

response = requests.get(api_url)

self.response = response.json()

def create_every_response(self):

self.format = date_switch[self.frequency]

api_url = self.header+self.page+"/data"+self.key+'&data[]='+self.data+'&frequency='+self.frequency

response = requests.get(api_url)

data = response.json()

final = data['response']['data']

total = data['response']['total']

offset = 5000

if total <= 5000:

self.response = final

else:

num_loops = math.floor(total/5000)

offset = 5000

for i in range(0,num_loops):

api_url = self.header+self.page+"/data"+self.key+'&data[]='+self.data+'&frequency='+self.frequency+'&offset='+str(offset)

response = requests.get(api_url)

data = response.json()

final += data['response']['data']

offset += 5000

percent = (offset-5000)/total*100

print("%.2f"%percent,'% of the way done')

self.response = final

def get_total_number_of_data_points(self):

api_url = self.header+self.page+"/data"+self.key+'&data[]='+self.data+'&frequency='+self.frequency

response = requests.get(api_url)

response = response.json()

return response['response']['total']

def create_df(self):

api_url = self.header+self.page+"/data"+self.key+'&data[]='+self.data+'&frequency='+self.frequency

response = requests.get(api_url)

data = response.json()

self.df = pd.DataFrame(data['response']['data'])

def return_url(self):

url = self.header+self.page+"/data"+self.key+'&data[]='+self.data+'&frequency='+self.frequency

return url

def create_data_df(self):

self.df = pd.DataFrame(self.response)

def create_index(self):

self.df['period'] = pd.to_datetime(self.df['period'],format = self.format)

self.df['time_idx'] = pd.DatetimeIndex(self.df['period'])

self.df = self.df.set_index('time_idx')

self.df = self.df.sort_values('time_idx')

def run_all(self):

self.load_page()

self.choose_frequency()

self.choose_data()

self.create_info()

self.create_every_response()

self.df = pd.DataFrame(self.response).drop_duplicates()

self.create_index()

print('Data has been obtained')

Building the Models

To build and determine the best model, I built the ForecastModel class below. A ForecastModel object takes four parameters: the data one wants to forecast which was pulled from the query, the number of past periods to train the models on, the number of periods to forecast, and the name of the column in the dataframe being passed that contains the data.

I perform a GridSearch across a Support Vector regressor, a XGBoost regressor, and a RandomForest regressor. First, I

To build the models, I first call the shift_values() method to shift the values being predicted up a row so that the features in each row will forecast the value for the next day. Next, I call train_models(), which calls the models and performs a GridSearch, trains each model on a 80/20 split, and then performs a forecast by using the datapoints forecasted as the features. I then store the error and the predictions for each model. Afterwards, I align the predictions with the dates they correspond to through update_df().

Finally, I call plot_best_model() to plot with the smallest MAE, while plot_data() plots all three models trained from the GridSearch. Calling find_best_model() works through the above steps and plots the best model. Calling the regressors attribute will display the final models created for each regressor. Below, I work through two examples.

params = {

'Support Vector Regressor':{"C": [0.5, 0.7], 'kernel':['rbf', 'poly']},

'RandomForest':{'max_features':[1.0,'sqrt'],'min_samples_split':[2,5,10],'min_samples_leaf':[1,2,4],'bootstrap':[True,False]},

'XGBoost':{'min_child_weight': [5, 7, 9],'colsample_bytree': [0.2, 0.4, 0.6],'max_depth': [5, 7, 9]}

}

class ForecastModel:

def __init__(self, df=None, num_shifts = None, num_predict = None, col = None,

error = None, test=None, predictions = None, final_df = None, final_date = None, first_date = None, regressors=None):

self.df = df

self.col = col

self.num_shifts = num_shifts

self.num_predict = num_predict

self.data = self.shift_values()

self.error = error

self.test = test

self.predictions = predictions

self.final_df = final_df

self.final_date = final_date

self.first_date = first_date

self.regressors = regressors

def create_regressors(self):

regressors = {

'Support Vector Regressor': [SVR()],

'RandomForest':[RandomForestRegressor()],

'XGBoost': [XGBRegressor()]

}

self.regressors = regressors

def shift_values(self):

df_dummy = self.df[[self.col]].copy()

for i in range(1,self.num_shifts+1):

name = self.col + "_shift " + str(i)

df_dummy[name] = df_dummy[self.col].shift(i)

df_dummy[self.col] = df_dummy[self.col].shift(-1)

df_dummy = df_dummy.dropna(how='any',axis=0)

y = df_dummy[self.col]

X = df_dummy.drop(self.col,axis=1)

return X,y

def train_models(self):

X,y = self.shift_values()

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, shuffle=False)

X_train = np.array(X_train)

X_test = np.array(X_test)

y_train = np.array(y_train)

y_test = np.array(y_test)

X_pred = X_test.copy()

self.create_regressors()

for reg in self.regressors:

print('Training '+reg)

model = self.regressors[reg][0]

#model.fit(X_train, y_train)

grid = GridSearchCV(model, params[reg])

grid.fit(X_train, y_train)

model = grid.best_estimator_

self.regressors[reg][0] = model

for i in range(0,len(X_pred)-1):

new = model.predict([X_pred[i]])

if i == 0:

predictions = np.array([new[0]])

else:

predictions = np.append(predictions,np.array([new[0]]))

X_pred[i+1] = np.concatenate([new,X_test[i+1][:-1]])

error = mean_absolute_error(y_test[:-1], predictions)

self.regressors[reg].append(error)

self.regressors[reg].append(predictions)

print(reg+' trained')

self.test = y_test

def update_df(self):

first_date = None

final_date = None

length = len(self.df[self.df[self.col] == self.test[0]].index)

for i in range(0,length):

x = self.df.index.get_loc(self.df[self.df[self.col] == self.test[0]].index[i])

new = x + len(self.test) - 1

if self.df.iloc[new]['value'] == self.test[-1]:

first_date = x

final_date = new + 1

break

self.first_date = first_date

self.final_date = final_date

self.final_df = self.df.iloc[first_date:final_date][[self.col]].copy()[:-1]

self.final_df['test'] = self.test[:-1]

for reg in self.regressors:

self.final_df[reg+' preds'] = self.regressors[reg][2]

def plot_best_model(self):

left = 500

right = 100

min_error = self.regressors['Support Vector Regressor'][1]

best_model_name = 'Support Vector Regressor'

for reg in self.regressors:

if self.regressors[reg][1] < min_error:

min_error = self.regressors[reg][1]

best_model_name = reg

rcParams['figure.figsize'] = 20,10

plt.plot(self.df[self.col], label = 'Full Dataset', color = 'black')

plt.plot(self.final_df[best_model_name+' preds'], label = best_model_name+' Predictions', color = 'blue')

corr = str(round(self.final_df.corr()[best_model_name+' preds']['value'],3))

min_error_name = ' MAE: %.3f' % min_error

plt.title(best_model_name+' Predictions r^2: '+corr+min_error_name)

plt.legend()

plt.show()

plt.plot(self.df[self.col][self.first_date - left:self.final_date + right], label = 'Previous', color = 'black')

plt.plot(self.final_df[best_model_name+' preds'], label = best_model_name+' Predictions', color = 'blue')

corr = str(round(self.final_df.corr()[reg+' preds']['value'],3))

plt.title(best_model_name+' Predictions r^2: '+corr+min_error_name)

plt.legend()

plt.show()

def find_best_model(self):

self.train_models()

self.update_df()

self.plot_best_model()

def plot_data(self):

left = 500

right = 100

for reg in self.regressors:

min_error = ' MAE: %.3f' % self.regressors[reg][1]

rcParams['figure.figsize'] = 20,10

plt.plot(self.df[self.col][self.first_date - left:self.final_date + right], label = 'Previous', color = 'black')

plt.plot(self.final_df[reg+' preds'], label = reg+' Predictions', color = 'blue')

corr = str(round(self.final_df.corr()[reg+' preds']['value'],3))

plt.title(reg+' Predictions r^2: '+corr+min_error)

plt.legend()

plt.show()

Forecasting Natural Gas Futures

Below, I walk through the process outlined above to forecast natural gas futures. Specifically, I will be forecasting the Contract 1 futures prices. Because natural gas contracts expire three business days prior to the first calendar day of the delivery month, Contract 1 contains the calendar month following the trade date. Information can be found at this link: https://www.eia.gov/dnav/ng/TblDefs/ng_pri_fut_tbldef2.asp.

Below, I create a LoadQuery object to pull the data that I want to forecast.

natural_gas_query = LoadQuery()

natural_gas_query.run_all()

Choose your id

id: coal Name: Coal

id: crude-oil-imports Name: Crude Oil Imports

id: electricity Name: Electricity

id: international Name: International

id: natural-gas Name: Natural Gas

id: nuclear-outages Name: Nuclear Outages

id: petroleum Name: Petroleum

id: seds Name: State Energy Data System (SEDS)

id: steo Name: Short Term Energy Outlook

id: densified-biomass Name: Densified Biomass

id: total-energy Name: Total Energy

id: aeo Name: Annual Energy Outlook

id: ieo Name: International Energy Outlook

id: co2-emissions Name: State CO2 Emissions

natural-gas

Choose your id

id: sum Name: Summary

id: pri Name: Prices

id: enr Name: Exploration and Reserves

id: prod Name: Production

id: move Name: Imports and Exports/Pipelines

id: stor Name: Storage

id: cons Name: Consumption / End Use

pri

Choose your id

id: sum Name: Natural Gas Prices

id: fut Name: Natural Gas Spot and Futures Prices (NYMEX)

id: rescom Name: Average Price of Natural Gas Delivered to Residential and Commercial Consumers by Local Distribution and Marketers in Selected States

fut

Choose the frequency

weekly

monthly

daily

annual

daily

11.82 % of the way done

23.64 % of the way done

35.46 % of the way done

47.28 % of the way done

59.10 % of the way done

70.92 % of the way done

82.74 % of the way done

94.56 % of the way done

Data has been obtained

Now that the data has been obtained, I call the dataframe to see the different features and how to filter for Contract 1.

natural_gas_query.df['series-description'].unique()

array(['Natural Gas Futures Contract 4 (Dollars per Million Btu)',

'Natural Gas Futures Contract 2 (Dollars per Million Btu)',

'Natural Gas Futures Contract 1 (Dollars per Million Btu)',

'Natural Gas Futures Contract 3 (Dollars per Million Btu)',

'Henry Hub Natural Gas Spot Price (Dollars per Million Btu)'],

dtype=object)

I will filter on the series description ‘Natural Gas Futures Contract 1 (Dollars per Million Btu)’.

series_desc = 'Natural Gas Futures Contract 1 (Dollars per Million Btu)'

natural_gas_data = natural_gas_query.df[(natural_gas_query.df['series-description'] == series_desc)]

natural_gas_data = natural_gas_data.dropna()

natural_gas_data.head()

| time_idx | period | duoarea | area-name | product | product-name | process | process-name | series | series-description | value | units |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1993-12-20 00:00:00 | 1993-12-20 00:00:00 | Y35NY | NEW YORK CITY | EPG0 | Natural Gas | PE4 | Future Contract 4 | RNGC4 | Natural Gas Futures Contract 4 (Dollars per Million Btu) | 1.894 | $/MMBTU |

| 1993-12-21 00:00:00 | 1993-12-21 00:00:00 | Y35NY | NEW YORK CITY | EPG0 | Natural Gas | PE4 | Future Contract 4 | RNGC4 | Natural Gas Futures Contract 4 (Dollars per Million Btu) | 1.83 | $/MMBTU |

| 1993-12-22 00:00:00 | 1993-12-22 00:00:00 | Y35NY | NEW YORK CITY | EPG0 | Natural Gas | PE4 | Future Contract 4 | RNGC4 | Natural Gas Futures Contract 4 (Dollars per Million Btu) | 1.859 | $/MMBTU |

| 1993-12-23 00:00:00 | 1993-12-23 00:00:00 | Y35NY | NEW YORK CITY | EPG0 | Natural Gas | PE4 | Future Contract 4 | RNGC4 | Natural Gas Futures Contract 4 (Dollars per Million Btu) | 1.895 | $/MMBTU |

| 1993-12-27 00:00:00 | 1993-12-27 00:00:00 | Y35NY | NEW YORK CITY | EPG0 | Natural Gas | PE4 | Future Contract 4 | RNGC4 | Natural Gas Futures Contract 4 (Dollars per Million Btu) | 1.965 | $/MMBTU |

I create the model by passing the dataframe natural_gas_data, train the model by having the previous 50 days predict the next day, forecast the next 150 days, and use the data in the column “value”.

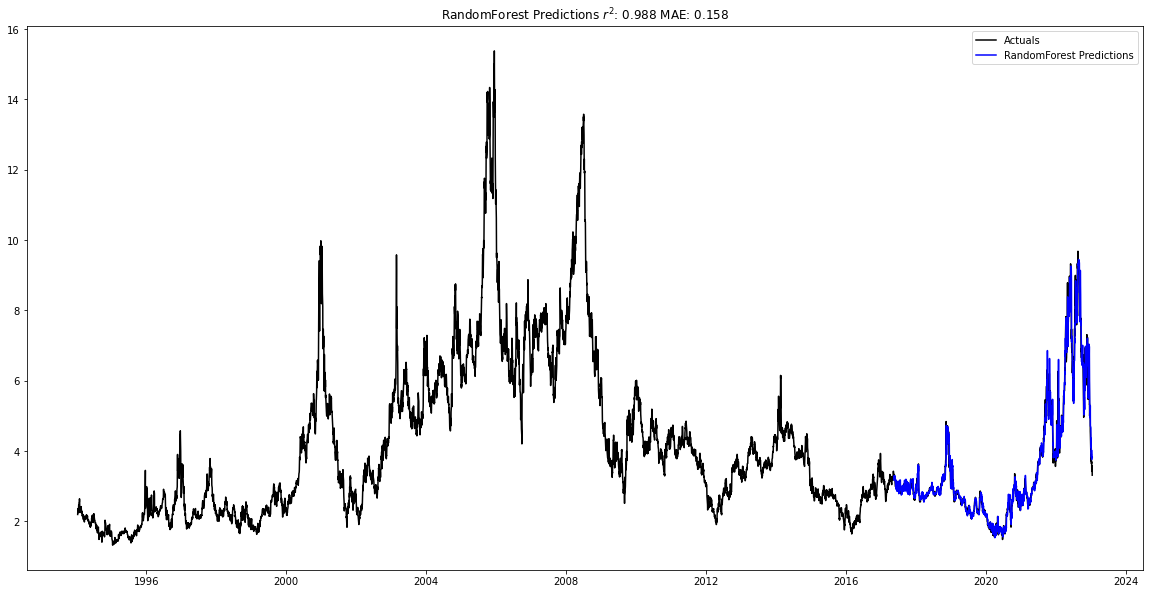

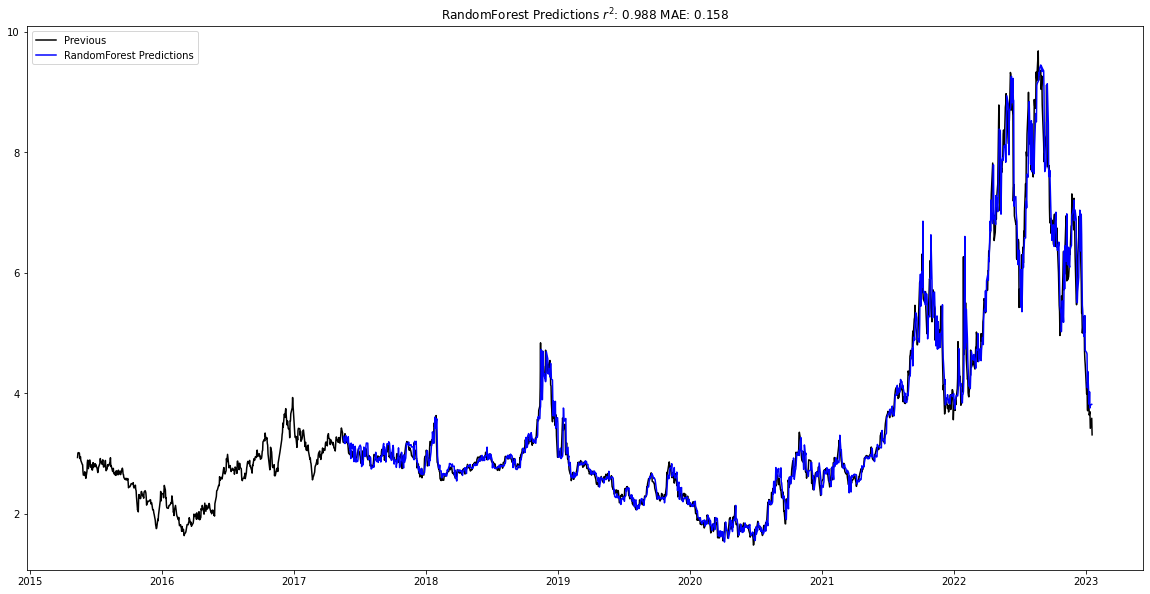

After training the models, the best model is graphed below. The Random Forest regressor was the best model, and had an r2 value of 0.988 with the testing data and a mean average error of 0.158.

natural_gas_forecast = ForecastModel(df = natural_gas_data, num_shifts = 50, num_predict = 150, col = 'value')

natural_gas_forecast.find_best_model()

Training Support Vector Regressor

Support Vector Regressor trained

Training RandomForest

RandomForest trained

Training XGBoost

XGBoost trained

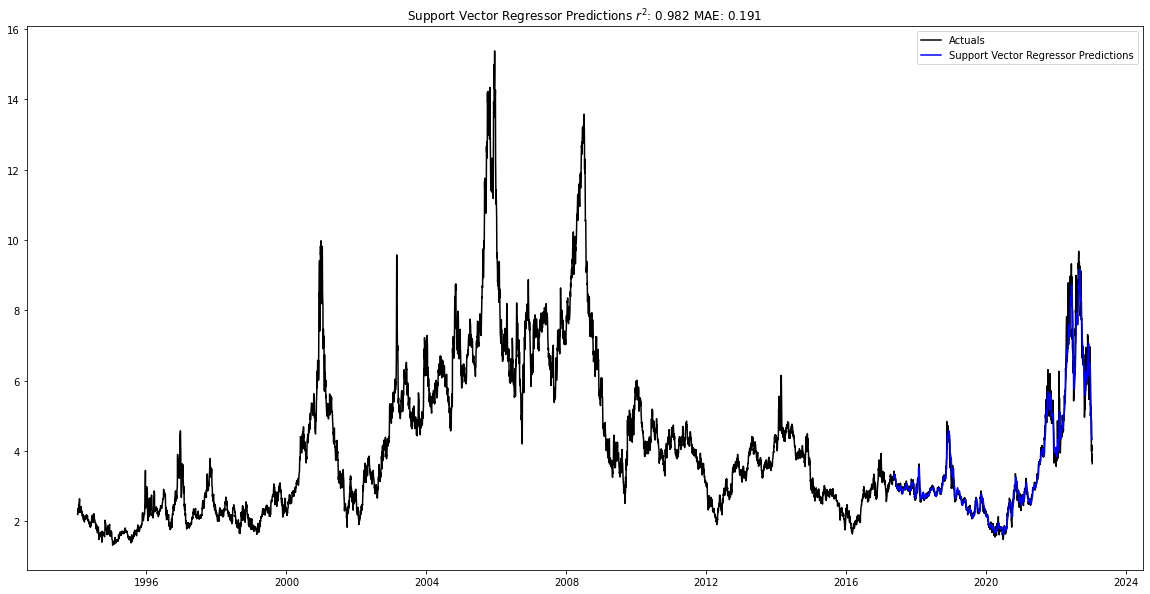

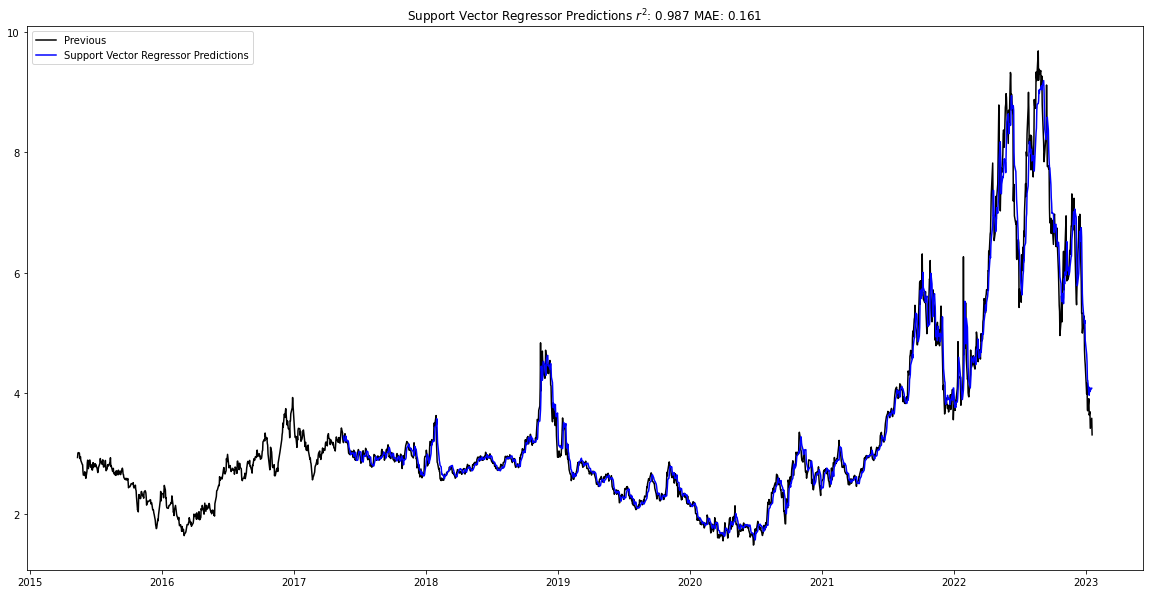

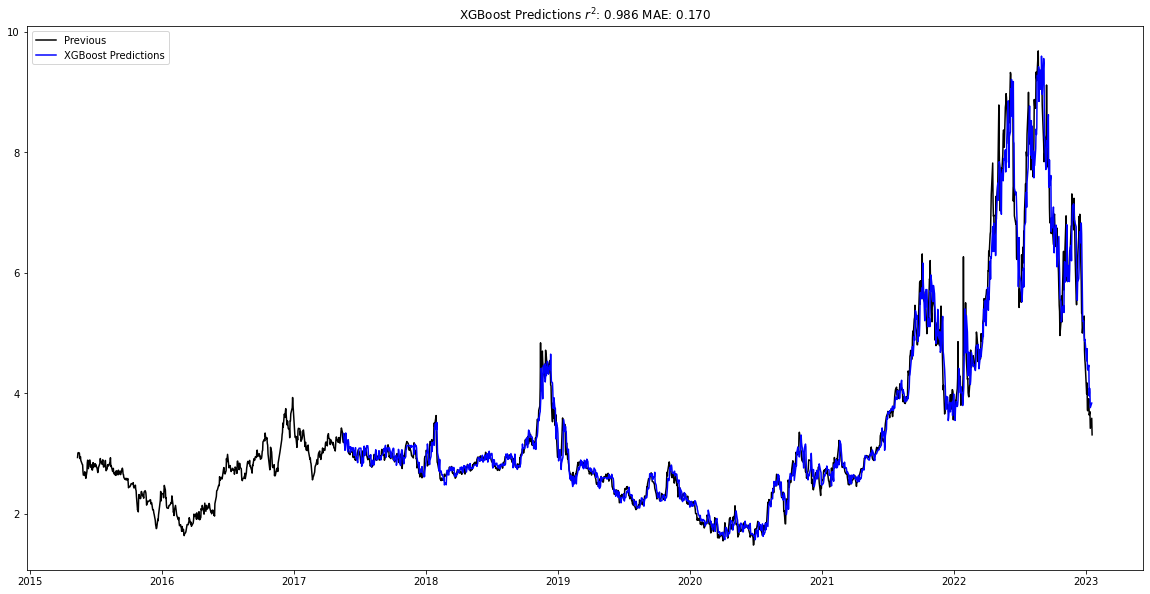

Below I plot the best predictions for each of the different regressors. In addition to the Random Forest regressor, the Support Vector regressor closely predicted the test data, with an r2 of 0.987 and an MAE of 0.161, as well as the XGBoost regression, which had an r2 of 0.986 and an MAE of 0.170.

natural_gas_forecast.plot_data()

Forecasting Petroleum Futures

I’ll now run through the same process by forecasting New York Harbor No. 2 Heating Oil Future Contract 1.

petroleum_forecast = LoadQuery()

petroleum_forecast.run_all()

Choose your id

id: coal Name: Coal

id: crude-oil-imports Name: Crude Oil Imports

id: electricity Name: Electricity

id: international Name: International

id: natural-gas Name: Natural Gas

id: nuclear-outages Name: Nuclear Outages

id: petroleum Name: Petroleum

id: seds Name: State Energy Data System (SEDS)

id: steo Name: Short Term Energy Outlook

id: densified-biomass Name: Densified Biomass

id: total-energy Name: Total Energy

id: aeo Name: Annual Energy Outlook

id: ieo Name: International Energy Outlook

id: co2-emissions Name: State CO2 Emissions

petroleum

Choose your id

id: sum Name: Summary

id: pri Name: Prices

id: crd Name: Crude Reserves and Production

id: pnp Name: Refining and Processing

id: move Name: Imports/Exports and Movements

id: stoc Name: Stocks

id: cons Name: Consumption/Sales

pri

Choose your id

id: gnd Name: Weekly Retail Gasoline and Diesel Prices

id: spt Name: Spot Prices

id: fut Name: NYMEX Futures Prices

id: wfr Name: Weekly Heating Oil and Propane Prices (October - March)

id: refmg Name: Refiner Gasoline Prices by Grade and Sales Type

id: refmg2 Name: U.S. Refiner Gasoline Prices by Formulation, Grade, Sales Type

id: refoth Name: Refiner Petroleum Product Prices by Sales Type

id: allmg Name: Gasoline Prices by Formulation, Grade, Sales Type

id: dist Name: No. 2 Distillate Prices by Sales Type

id: prop Name: Propane (Consumer Grade) Prices by Sales Type

id: resid Name: Residual Fuel Oil Prices by Sales Type

id: dfp1 Name: Domestic Crude Oil First Purchase Prices by Area

id: dfp2 Name: Domestic Crude Oil First Purchase Prices for Selected Crude Streams

id: dfp3 Name: Domestic Crude Oil First Purchase Prices by API Gravity

id: rac2 Name: Refiner Acquisition Cost of Crude Oil

id: imc1 Name: F.O.B. Costs of Imported Crude Oil by Area

id: imc2 Name: F.O.B. Costs of Imported Crude Oil for Selected Crude Streams

id: imc3 Name: F.O.B. Costs of Imported Crude Oil by API Gravity

id: land1 Name: Landed Costs of Imported Crude by Area

id: land2 Name: Landed Costs of Imported Crude for Selected Crude Streams

id: land3 Name: Landed Costs of Imported Crude by API Gravity

id: ipct Name: Percentages of Total Imported Crude Oil by API Gravity

fut

Choose the frequency

weekly

daily

monthly

annual

daily

3.68 % of the way done

7.36 % of the way done

11.05 % of the way done

14.73 % of the way done

18.41 % of the way done

22.09 % of the way done

25.78 % of the way done

29.46 % of the way done

33.14 % of the way done

36.82 % of the way done

40.50 % of the way done

44.19 % of the way done

47.87 % of the way done

51.55 % of the way done

55.23 % of the way done

58.91 % of the way done

62.60 % of the way done

66.28 % of the way done

69.96 % of the way done

73.64 % of the way done

77.33 % of the way done

81.01 % of the way done

84.69 % of the way done

88.37 % of the way done

92.05 % of the way done

95.74 % of the way done

99.42 % of the way done

Data has been obtained

petroleum_forecast.df.head()

| time_idx | period | duoarea | area-name | product | product-name | process | process-name | series | series-description | value | units |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1980-01-02 00:00:00 | 1980-01-02 00:00:00 | Y35NY | NEW YORK CITY | EPD2F | No 2 Fuel Oil / Heating Oil | PE1 | Future Contract 1 | EER_EPD2F_PE1_Y35NY_DPG | New York Harbor No. 2 Heating Oil Future Contract 1 (Dollars per Gallon) | 0.821 | $/GAL |

| 1980-01-02 00:00:00 | 1980-01-02 00:00:00 | Y35NY | NEW YORK CITY | EPD2F | No 2 Fuel Oil / Heating Oil | PE3 | Future Contract 3 | EER_EPD2F_PE3_Y35NY_DPG | New York Harbor No. 2 Heating Oil Future Contract 3 (Dollars per Gallon) | 0.89 | $/GAL |

| 1980-01-03 00:00:00 | 1980-01-03 00:00:00 | Y35NY | NEW YORK CITY | EPD2F | No 2 Fuel Oil / Heating Oil | PE1 | Future Contract 1 | EER_EPD2F_PE1_Y35NY_DPG | New York Harbor No. 2 Heating Oil Future Contract 1 (Dollars per Gallon) | 0.827 | $/GAL |

| 1980-01-04 00:00:00 | 1980-01-04 00:00:00 | Y35NY | NEW YORK CITY | EPD2F | No 2 Fuel Oil / Heating Oil | PE3 | Future Contract 3 | EER_EPD2F_PE3_Y35NY_DPG | New York Harbor No. 2 Heating Oil Future Contract 3 (Dollars per Gallon) | 0.88 | $/GAL |

petroleum_forecast.df['series-description'].unique()

array(['New York Harbor No. 2 Heating Oil Future Contract 3 (Dollars per Gallon)',

'New York Harbor No. 2 Heating Oil Future Contract 1 (Dollars per Gallon)',

'Cushing, OK Crude Oil Future Contract 3 (Dollars per Barrel)',

'Cushing, OK Crude Oil Future Contract 1 (Dollars per Barrel)',

'New York Harbor Regular Gasoline Future Contract 3 (Dollars per Gallon)',

'New York Harbor Regular Gasoline Future Contract 1 (Dollars per Gallon)',

'Cushing, OK Crude Oil Future Contract 2 (Dollars per Barrel)',

'Cushing, OK Crude Oil Future Contract 4 (Dollars per Barrel)',

'Mont Belvieu, Tx Propane Future Contract 1 (Dollars per Gallon)',

'Mont Belvieu, Tx Propane Future Contract 4 (Dollars per Gallon)',

'New York Harbor No. 2 Heating Oil Future Contract 4 (Dollars per Gallon)',

'New York Harbor Regular Gasoline Future Contract 2 (Dollars per Gallon)',

'New York Harbor Regular Gasoline Future Contract 4 (Dollars per Gallon)',

'New York Harbor No. 2 Heating Oil Future Contract 2 (Dollars per Gallon)',

'Mont Belvieu, Tx Propane Future Contract 2 (Dollars per Gallon)',

'Mont Belvieu, Tx Propane Future Contract 3 (Dollars per Gallon)',

'New York Harbor Reformulated RBOB Regular Gasoline Future Contract 2 (Dollars per Gallon)',

'New York Harbor Reformulated RBOB Regular Gasoline Future Contract 1 (Dollars per Gallon)',

'New York Harbor Reformulated RBOB Regular Gasoline Future Contract 4 (Dollars per Gallon)',

'New York Harbor Reformulated RBOB Regular Gasoline Future Contract 3 (Dollars per Gallon)'],

dtype=object)

petreoleum_forecast_data.df = petroleum_forecast.df[petroleum_forecast.df['series-description'] == 'New York Harbor No. 2 Heating Oil Future Contract 1 (Dollars per Gallon)']

petreoleum_forecast_data.df = petreoleum_forecast_data.df.dropna()

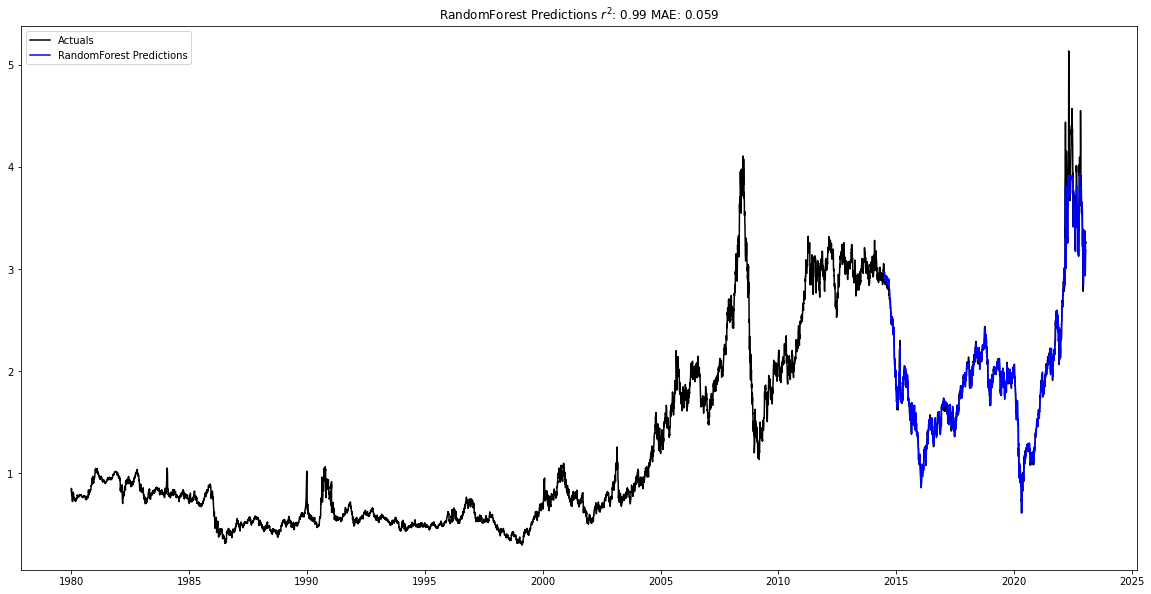

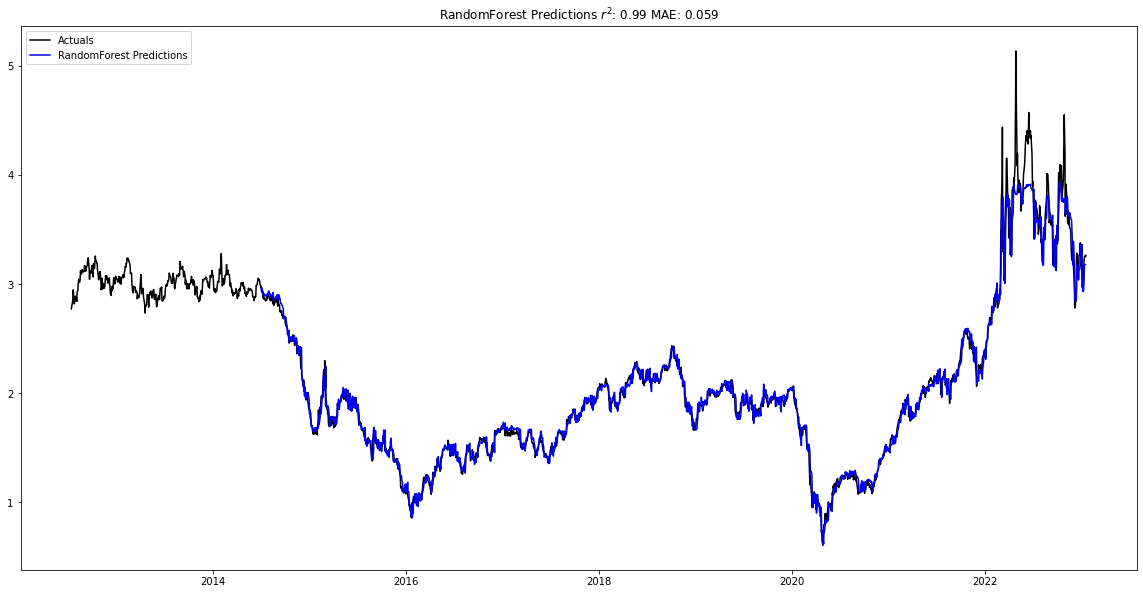

After training the different models, the Random Forest regressor again the smallest MAE at 0.058 and the largest r2 at 0.99 for the testing data.

petroleum_forecast_model = ForecastModel(df = petreoleum_forecast_data.df, num_shifts = 50, num_predict = 150, col = 'value')

petroleum_forecast_model.find_best_model()

Training Support Vector Regressor

Support Vector Regressor trained

Training RandomForest

RandomForest trained

Training XGBoost

XGBoost trained

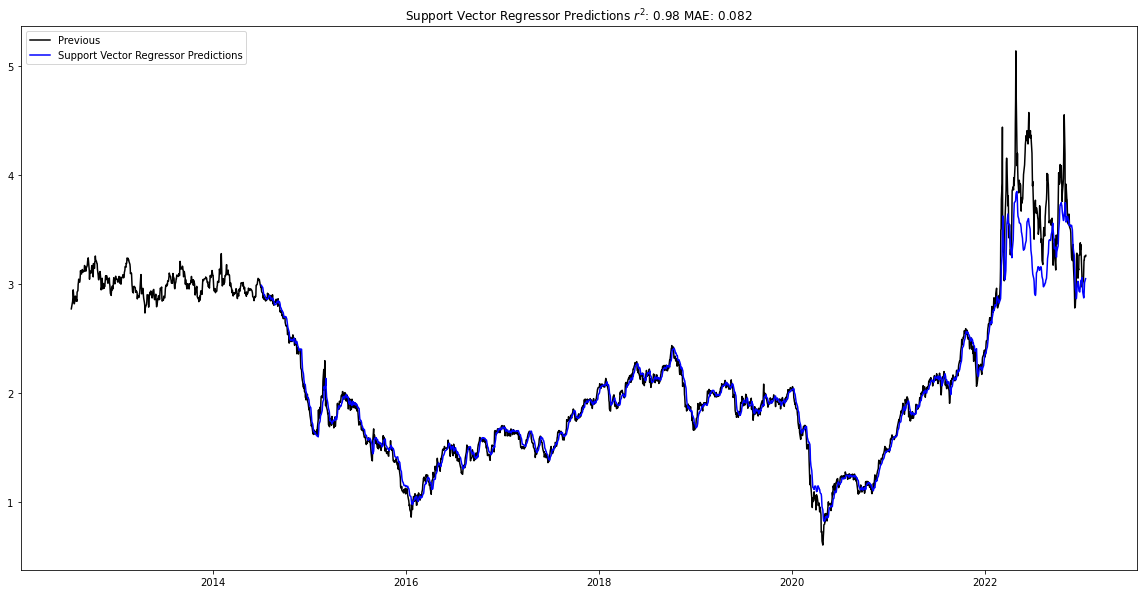

Looking at the other the models, we see that the Support Vector regressor and the XGBoost regressor also captured the trend.

petroleum_forecast_model.plot_data()

Conclusions and Next Steps

Taking a look at the natural gas and petroleum futures predictions, we are able to see that the models captured the volatility due to the Covid-19 pandemic and the invasion of Ukraine in their forecasting fairly well. Although the petroleum forecasts had more difficulty during the invasion of Ukraine, the Random Forest model captured the overall movement. To address this, a model that includes news events could be helpful, as I discuss below. As a result, it seems that univariate time-series models can be useful and cost-effective in forecasting markets in the short term.

I believe that there are several ways to improve this project. First, when testing the models across other datasets, some models were more seasonal than the data shown above. As a result, when data appears more seasonal, performing a seasonality decomposition could increase model performance while decreasing complexity. Secondly, there were some datasets where models had more difficulty making predictions. Creating a multivariate model that incorporates features such as GDP, local and international conflicts, different weather events, and location could improve model performance as well. Finally, this model only included 1 period forecasts. It would be interesting to see how this approach fares in predicting multi-period forecasts, such as a 7 day forecast or a 30 day forecast. To accomplish this, including an RNN neural net model could be helpful in creating these forecasts.